Let’s talk about Biden’s proposed tax policies and how they will affect the individual taxpayer. There are ten key proposed changes that I want to discuss. Keep in mind these are all just proposals, Biden is not even president yet, and these have to pass through Congress for them to become law. I am sure there is going to be pushback from the Republicans because some of these tax increases are significant for the wealthy, but most Americans will not be affected by the increases.

Tax Brackets

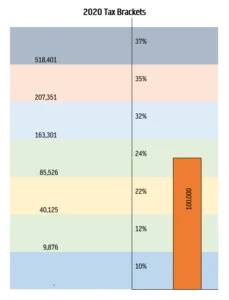

I want to start by explaining how the tax bracket works because there have been a lot of misconceptions about tax brackets. The table inserted below shows the 2020 tax brackets.

Looking at the table above if you make between $0 and $9,875 that money would be taxed at 10%. Your earnings from $9,876 to $40,124 would be taxed at 12%, earnings from $40,125 to $85,525 would be taxed at 22%, and on and on up to the 37% top tax bracket. Here is where there is a misconception, let’s say we have somebody making $100,000 a year gross, the misconception is that that entire $100,000 will be taxed at 24%. And that is simply not true. What happens is the first portion, between $0 and $9,875 is taxed at 10%, then the second portion up to $40,124 is taxed at 12%, the third portion up to $85,525 is taxed at 22%, and then the very last marginal portion from $85,526 to $100,00 is taxed at 24%. That is basically how marginal tax brackets work. So, if you happen to jump into the next tax bracket, you are not going to end up paying significantly more taxes on your entire income, you are taxed at the higher rate only on the amount that jumps over that tax bracket. With that understanding, let’s get into some of the changes Joe Biden is proposing.

Increasing the Top Tax Bracket

The first major change in Biden’s proposal is to increase the top tax bracket from 37% to 39.6%. Before the Trump Tax Reform, this top bracket was 39.6% so this really is not a big deal. Biden is not proposing changing any of the other tax brackets currently.

Social Security Tax

The second major change in Biden’s proposal is a 12.4% social security tax on income over $400,000. All employees earning a W2 wage are already paying social security tax. 6.2% of the 12.4% social security tax comes directly out of your paycheck and the other 6.2% is paid by your employer. That social security tax drops off when you get to an income of $137,700. In Biden’s proposed plan that social security tax will pick back up once you hit the $400,000 income limit. This is called a “donut hole”. A donut hole meaning you are taxed up to a certain point and then you are not taxed until you get to a higher income level. This will affect W2 employees that earn a high income and the self-employed. If you earn W2 wages your employer will pay half and the other half will be deducted from your paycheck. If you are self-employed, you are paying the full 12.4%.

Long-Term Capital Gains Rate

The third major change in Biden’s proposal is increasing the long-term capital gains rate up to the ordinary income tax rate of 39.6% for people making over $1,000,000 of income. $1,000,000 of income from capital gains is a lot of capital gains income. This probably will not apply to most Americans. But good to note either way because that is a huge increase. The top tax rate for long-term capital gains right now is 23.8% so jumping from 23.8% to 39.6% is a huge increase.

Removal of the Step-up in Cost Basis

The fourth major change in Biden’s proposal is the removal of the step-up in cost basis for capital assets. The best way to explain this is to give you an example. If you purchase a home for $100,000, that $100,00 is your cost basis. When you sell that home, you are going to take your selling price minus your cost basis ($100,000) to determine your capital gains. You then pay taxes on those capital gains. Under the current laws, if you buy a home for $100,000 and hold on to it for 50 years, you die, and your children inherit the house. The current value of the house is now $500,000. Whoever inherits that home, will get their cost basis stepped up to $500,000. That means when they sell the home, their capital gains tax will be calculated based on the $500,000 not the original $100,000. Biden’s proposal will eliminate that and the capital gains and associated capital gains taxes will be based on the original $100,000 cost basis. This will have a significant effect on estate planning.

Capping Itemized Deductions

The fifth major change in Biden’s proposal is a cap on itemized deduction benefits at 28%. This will only affect those earning income above the 28% tax bracket. Under the current law, if you are in the 32% – 37% tax bracket, every dollar that you deduct from your taxable income comes with a 32% – 37% benefit in terms of reducing your taxes accordingly. Biden is proposing to cap that benefit at 28%.

The Pease Limitation

The sixth major change in Biden’s proposal is bringing back the Pease limitation on itemized deductions. This reduces the power of itemized deductions by another 3% if you make over $400,000.

Decrease in the Estate Tax Exclusion

The seventh major change in Biden’s proposal is decreasing the estate tax exclusion to $3.5 million per individual. This is huge. This will primarily affect the extremely wealthy but what it means is if you die with an estate value of over $3.5 million then you are going to have to pay estate taxes on those assets. This will be another big change for the estate planning industry.

Increase the Child Dependent Care Credit

The eighth major change in Biden’s proposal is an increase in the child dependent care tax credit. When you pay for childcare throughout the year, you get to claim that childcare as a tax credit. Biden’s proposal increases some of the limits to give you a better tax credit.

Increase to the Child Tax Credit

The ninth change in Biden’s proposal is an increase in the child tax credit. The child tax credit is a credit you take for any child, 17 years or younger, that you claim as a dependent. The current amount of this credit is $2,000. Biden’s proposal will increase that credit to $3,000 per child with an additional $600 for any child 6 years old and under. This is a significant increase from the current $2,000 credit.

First Time Home Buyer Tax Credit

The final major change in Biden’s proposal is the first-time homebuyer tax credit. This tax credit is going to be $15,000 for first-time home buyers. This is a significant tax credit so something to think about if you are considering purchasing your first home.Those are the 10 major changes that Biden is proposing. How can you prepare for them now?

- Get your retirement funds into the right accounts. Now would be a good time to consider switching your accounts to Roth accounts. Converting from a traditional IRA or 401K means you pay the taxes at the time of conversion instead of when you access the funds to use them for your retirement. Basically, you are “locking in” at the current lower tax rate.

- Meet with an estate planning attorney, especially if you are closer to retirement. If you have a bunch of assets or property you want to make sure your ducks are in a row. Get with an estate planning attorney and make sure you are set up properly just in case these tax laws change.

- If you are currently paying for childcare and you are not keeping track of how much you are paying, start now. If you do not have information on the childcare center or your nanny, get that information so that you can take advantage of the child dependent care tax credit. There is a form W10 that you can have your nanny fill out that gives you the information you need or if you use a childcare center or preschool, make sure you get a tax ID statement from them at the end of the year.

- If you own a small business, this would be a good time to evaluate how your entity is set up and how it is taxed. I usually recommend that you have your business structured as an LLC. But now because of the proposed increase in social security tax, if you are self-employed, that is going to cost you a lot of money if your business is successful.

We are here to help. If you need assistance, reach out to us at nguyencpas.com or support@nguyencpas.com and schedule a complimentary consultation with one of our advisors.